Quick Answer

Venture capitalists expect most startups to fail because venture investing is built on outlier returns, not average outcomes.

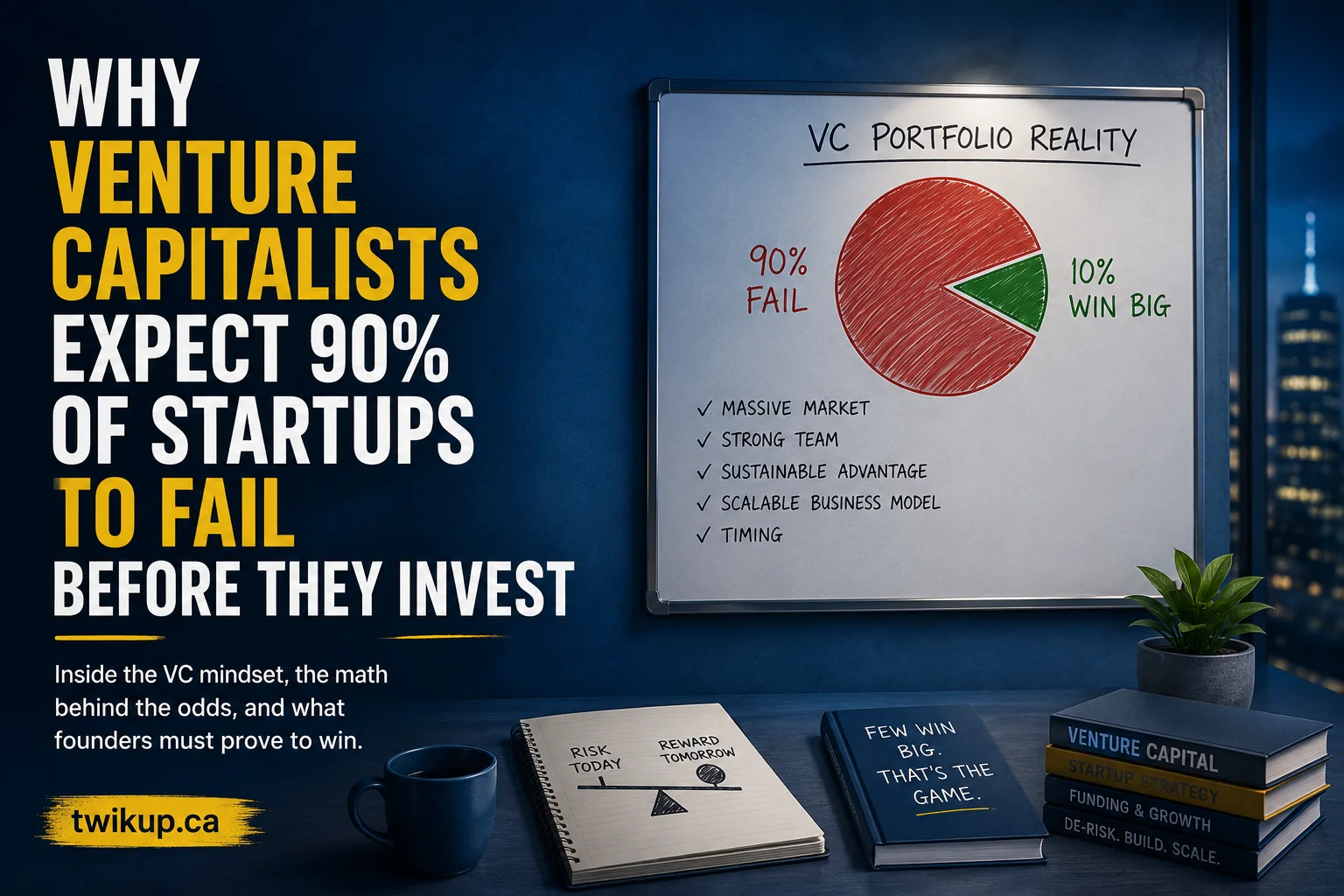

A VC does not invest because every startup looks safe. They invest because one or two companies in a portfolio can become large enough to repay the losses from many failed bets. Research often shows that around 75% of venture-backed startups fail to return investor capital, while broader startup failure statistics vary depending on how “failure” is defined. Harvard Business School

That is why VCs ask hard questions before investing:

Can this become a billion-dollar company?

Can the market get very large?

Can the founder survive pressure?

Can this startup grow fast enough to justify venture-scale risk?

TwikUp Insight

Most founders think VC funding is about proving their startup will not fail.

But venture capitalists are usually asking a different question:

“If this works, can it become big enough to make the risk worth it?”

That is the real game. VCs already know many startups will fail. They are not looking for safe small wins. They are looking for rare breakout companies that can return the fund.

For founders, this means one important thing: do not pitch like a small business. Pitch like a company that can dominate a large market.

Why VCs Expect Startups to Fail Before They Invest

The famous line “90% of startups fail” is popular because it captures the emotional truth of entrepreneurship: most startups do not become big companies.

But the real picture is more nuanced.

According to U.S. Bureau of Labor Statistics data, many new businesses survive the first year, but survival drops over time. One BLS analysis found that only 34.7% of private-sector establishments born in March 2013 were still operating in March 2023. BLS

For venture-backed startups, the bar is even higher. A startup can still exist and still be a “failure” for VC purposes if it does not return enough capital to investors.

That is why Harvard Business School research often cited in the VC world says about three-quarters of venture-backed startups fail to return investors’ capital. HBS

In simple words:

A normal business can survive and be useful.

A VC-backed startup must become very big, very fast.

That difference changes everything.

The VC Business Model Is Built on the Power Law

Venture capital does not work like buying a stable dividend stock or a profitable local business.

VC works on the power law.

That means a small number of investments can create most of the returns. One winner can matter more than every failed investment combined.

For example, if a VC fund invests in 30 startups, the outcome may look something like this:

| Portfolio Outcome | What Usually Happens |

|---|---|

| Many startups | Fail or return little capital |

| Some startups | Return 1x–3x |

| Very few startups | Become major winners |

| One breakout startup | Can return a large part of the fund |

This is why VCs are comfortable with failure. They are not trying to avoid every loss. They are trying to find the one company that can become massive.

This connects directly with founder valuation. If you want to understand how investors think about upside, read: Your Startup Isn’t Worth What You Think—Here’s How Investors Actually Value It.

Why “Failure” Means Something Different to a VC

A startup may look successful from the outside:

- It raised money

- It hired employees

- It built a product

- It got customers

- It survived for years

But for a venture capitalist, that may still not be enough.

VCs invest money from limited partners such as pension funds, university endowments, family offices, fund-of-funds and wealthy investors. They are expected to return far more than the original capital.

So if a startup raises $10 million and later sells for $20 million, that may sound good. But after liquidation preferences, dilution, debt, legal costs and investor rights, common shareholders and even some investors may not make much.

This is why fundraising can create pressure after the round closes. For a deeper breakdown, read: You Raised Millions—Here’s What Happens Next and Where Many Founders Go Wrong.

The Main Reasons Startups Fail

CB Insights analyzed hundreds of startup post-mortems and found recurring failure patterns, including running out of cash, weak market demand, poor timing, pricing issues, competition and team problems. CB Insights

The biggest lessons are simple:

1. The Market Was Not Big Enough

VCs do not just ask, “Is this a good idea?”

They ask, “Can this become a huge company?”

A startup solving a small problem may be a good business, but not a venture-scale company. If the market is too small, even great execution may not produce VC-level returns.

2. Customers Did Not Need It Badly Enough

Founders often confuse interest with demand.

People may say the idea is interesting. They may even try the product. But if they do not pay, return, recommend or switch behavior, the startup may not have real product-market fit.

That is why investors often say no even when they like the founder or the idea. Read: Why Investors Say No Even When They Like Your Startup.

3. The Startup Ran Out of Cash

Many startups do not fail because the idea was terrible. They fail because they run out of time.

Cash burn, hiring, marketing costs, product delays and slow revenue can kill a startup before the market proves itself.

This is why VCs care about runway, burn multiple, gross margin and fundraising milestones.

4. The Team Could Not Handle the Pressure

Startups are not only product problems. They are people problems.

Founder conflict, weak hiring, poor decision-making and lack of focus can destroy a company faster than competition.

VCs know this, which is why they evaluate founder psychology, speed, resilience and honesty before investing.

5. The Company Could Not Scale

Some startups find early customers but cannot scale profitably.

The product works manually, but not operationally. Sales depend too much on the founder. Customer acquisition costs rise. Margins shrink. Support becomes expensive.

That is when a promising startup becomes a difficult investment.

Why VCs Still Invest Despite the Risk

The simple answer: because the upside can be enormous.

A traditional investor may want predictable cash flow. A venture capitalist wants asymmetric upside.

If a VC invests $1 million into a startup that becomes worth $1 billion, that one investment can change the entire fund.

That is why VCs are willing to accept failure rates that would look unacceptable in other asset classes.

The goal is not to be right every time.

The goal is to be right enough on one or two massive winners.

What VCs Look for Before Taking the Risk

Before investing, venture capitalists usually look for five things:

1. A Large Market

The market must be big enough to support a venture-scale outcome.

A $50 million market may support a good business. A multi-billion-dollar market can support a VC-backed company.

2. A Strong Founder-Market Fit

VCs want founders who deeply understand the problem.

This can come from industry experience, personal pain, technical insight or a unique distribution advantage.

3. Evidence of Pull

Investors like signs that customers are pulling the product into the market.

Examples include:

- Fast user growth

- Strong retention

- Revenue momentum

- High customer urgency

- Organic referrals

- Low churn

- Repeat usage

4. A Path to Defensibility

VCs want to know why the company can win long term.

Defensibility may come from data, network effects, brand, distribution, technology, regulation, switching costs or operational complexity.

5. A Fund-Returning Outcome

This is the biggest point founders miss.

A VC is not only asking, “Can this startup succeed?”

They are asking, “Can this investment return enough to matter to my fund?”

That is why a decent business can still be rejected.

For the full fundraising journey, read: The Complete Startup Fundraising Roadmap: From Idea to IPO.

Why This Matters for Founders

If you are raising venture capital, you need to understand the investor’s mindset.

A VC already assumes risk. Your job is not to pretend there is no risk.

Your job is to show that the upside is worth the risk.

That means your pitch should clearly explain:

- Why this problem matters now

- Why the market is large

- Why your team can win

- Why customers care

- Why this can scale

- Why the timing is right

- Why this could become a category leader

The worst pitch says: “This is a safe business.”

The stronger pitch says: “This is risky, but if we are right, this can become very large.”

The Hidden Trade-Off: VC Money Comes With Control

When a startup raises VC money, the founder is no longer building alone.

Investors may receive board seats, preferred shares, protective rights and influence over major decisions.

That does not mean VCs are bad. It means venture funding changes the company’s governance.

If growth slows, the board may push for leadership changes, cost cuts, a sale, a pivot or a new CEO.

Founders should understand this before taking capital, not after. Read: Your Board Can Fire You: What Every Founder Should Know After Raising Capital.

Founder Takeaway

VCs expect many startups to fail because venture capital is not built around average outcomes. It is built around rare, extreme winners.

That is why investors reject many good ideas, push for large markets, ask uncomfortable questions and focus so heavily on scale.

For founders, the lesson is clear:

Do not raise venture capital just because it sounds prestigious.

Raise it only if your startup has the potential, ambition and market size to become a very large company.

Because once you take VC money, the game changes.

You are no longer just trying to survive.

You are trying to become big enough to make the risk worth it.