Canada Mortgage Rate Prediction 2026–2030: Will Rates Fall Again—or Is 4% the New Normal?

For years, Canadian homebuyers became accustomed to one simple idea: when the economy weakens, interest rates fall and mortgages eventually become cheaper.

But the next five years may not be that simple.

Canada is entering an unusual economic period.

The economy faces pressure from trade uncertainty, tariffs, slower investment and an uncertain job market. Normally, those conditions would increase pressure on the Bank of Canada to lower interest rates.

At the same time, higher energy prices, geopolitical conflicts and the risk of renewed inflation could prevent rates from falling too far.

That leaves Canadian homebuyers, homeowners and investors facing one important question:

Will mortgage rates finally fall again between 2026 and 2030—or could rates around 4% become the new normal in Canada?

The answer may depend on which force becomes stronger: Canada’s weakening economy or the return of inflation.

Important: This article contains economic analysis and scenario-based projections for educational and informational purposes only. Mortgage rates cannot be predicted with certainty. Actual rates will depend on future Bank of Canada decisions, bond markets, lender pricing, inflation and economic conditions. This article is not financial, mortgage or investment advice.

Quick Answer

Canadian mortgage rates could move lower between 2026 and 2030, but a permanent return to the ultra-low mortgage rates seen during the pandemic is unlikely under normal economic conditions.

As of June 2026, the Bank of Canada’s policy rate was 2.25%. Competitive five-year variable mortgage rates were around the mid-3% range, while some competitive five-year fixed rates were around 4%.

Our base-case scenario is that Canadian mortgage rates spend much of the 2026–2030 period fluctuating within a broad 3.5% to 5% range, although rates could temporarily move below or above that level.

A severe recession and major job losses could push rates lower.

Persistent inflation, higher oil prices or another global supply shock could push rates higher.

The most important takeaway? Canadians waiting for 2% mortgages to become normal again could be waiting for something that never happens.

For buyers trying to understand how rates translate into real monthly costs, Twikup’s guide to mortgage payments on a $500K, $700K and $1 million home in Canada is a useful next read.

Key Takeaways

- The Bank of Canada held its policy interest rate at 2.25% in June 2026.

- Canada’s economy faces pressure from U.S. tariffs, trade uncertainty and weaker investment.

- The unemployment rate fell to 6.6% in May 2026, but the labour market remains an important factor to watch.

- Higher oil and energy prices could keep inflation elevated and make aggressive rate cuts more difficult.

- Variable mortgage rates are more directly influenced by Bank of Canada policy decisions.

- Fixed mortgage rates are heavily influenced by Government of Canada bond yields and lender funding costs.

- Mortgage rates do not necessarily fall immediately when the Bank of Canada cuts interest rates.

- Twikup’s base-case scenario is that mortgage rates could spend much of 2026–2030 between approximately 3.5% and 5%.

- A return to 2% mortgages is possible during a major economic crisis, but it should not be treated as the most likely long-term outcome.

Where Do Canadian Mortgage Rates Stand in 2026?

Before predicting mortgage rates through 2030, it is important to understand where Canada stands today.

In June 2026, the Bank of Canada maintained its policy interest rate at 2.25%.

At the same time, competitive Canadian mortgage rates showed an important divide.

Five-year variable mortgage rates were available around the mid-3% range, while some competitive five-year fixed mortgage rates remained around 4%.

Why the difference?

Because fixed and variable mortgage rates do not move in exactly the same way.

| Rate | Main Influence |

|---|---|

| Bank of Canada policy rate | Inflation and the Canadian economy |

| Prime rate | Bank of Canada policy decisions |

| Variable mortgage rates | Prime rate and lender discounts |

| Fixed mortgage rates | Government bond yields and lender funding costs |

This distinction is critical when predicting Canadian mortgage rates.

The Bank of Canada could lower its policy rate without causing five-year fixed mortgage rates to fall by the same amount.

That is one reason Canadians waiting for dramatically cheaper mortgages could be disappointed.

The Biggest Question: Is 4% the New Normal for Canadian Mortgages?

This is the central question facing Canada’s housing market.

During the pandemic, some Canadian borrowers secured mortgage rates below 2%.

Those rates transformed what Canadians believed was “normal.”

But historically, borrowing money at extremely low rates was an unusual situation created by extraordinary economic circumstances.

The next five years could look very different.

Instead of mortgage rates continuously falling, Canada could enter an environment where rates move up and down within a relatively stable range.

For example:

- Economic weakness pushes rates toward 3%.

- Economic recovery pushes rates higher.

- Inflation keeps rates from falling too far.

- A recession temporarily creates lower borrowing costs.

- Higher oil prices or supply shocks push rates upward again.

This creates the possibility that mortgage rates around 4% become the middle ground rather than an unusually high rate.

This also matters for housing prices. If rates stay near 4% instead of returning to 2%, the next phase of Canadian real estate may look very different from the last decade. For a broader price outlook, read Twikup’s Canada real estate price prediction for 2026–2031.

The Bank of Canada Is Caught Between Two Very Different Problems

Understanding the 2026–2030 mortgage rate outlook becomes much easier when you look at the Bank of Canada’s challenge.

The Bank is essentially caught between two competing risks.

Risk #1: Canada’s economy becomes too weak.

That could mean:

- rising unemployment;

- significant job losses;

- weaker consumer spending;

- businesses delaying investment;

- falling housing activity;

- tariff-related economic damage.

These conditions could increase pressure to lower interest rates.

Risk #2: Inflation returns.

That could mean:

- higher oil prices;

- rising gasoline prices;

- global conflict;

- supply-chain disruption;

- tariffs increasing business costs;

- broader price pressures.

These conditions could prevent the Bank of Canada from cutting rates—or potentially create pressure for rates to rise.

The direction of Canadian mortgage rates could depend on which of these two risks becomes more serious.

Why Canadian Mortgage Rates Could Fall

1. Canada’s Job Market Could Weaken

The job market will likely be one of the most important indicators for future interest rates.

Canada’s unemployment rate fell to 6.6% in May 2026, while employment increased by 88,000 during the month.

That was a positive development.

However, one month does not determine the long-term direction of the economy.

If unemployment begins rising consistently and businesses start cutting jobs, Canadian households could reduce spending.

That would weaken economic demand.

A serious labour-market downturn could increase pressure on the Bank of Canada to reduce interest rates.

What should Canadians watch?

Pay attention to:

- unemployment;

- monthly job creation;

- youth unemployment;

- wage growth;

- job vacancies;

- business hiring intentions.

If these indicators deteriorate significantly, the probability of lower interest rates could increase.

2. The Canadian Economy Could Remain Weak

Canada continues to adjust to major changes in the global economy.

U.S. tariffs and trade uncertainty are affecting the outlook for Canadian businesses.

When companies are uncertain about future trade relationships, they may delay:

- hiring;

- factory expansions;

- equipment purchases;

- new investments.

Lower business investment can weaken economic growth.

If Canada enters a prolonged period of slow growth, the Bank of Canada could eventually face pressure to provide additional support through lower interest rates.

3. Canadian Households Are Highly Sensitive to Interest Rates

Canada has another important vulnerability: household debt.

Millions of homeowners must regularly renew their mortgages.

Borrowers who previously secured extremely low rates could face significantly higher monthly payments when renewing.

Higher mortgage payments can reduce the amount households spend elsewhere.

A family paying hundreds of dollars more each month toward its mortgage may spend less on:

- restaurants;

- travel;

- vehicles;

- renovations;

- entertainment;

- retail purchases.

If this happens across millions of households, consumer spending could weaken.

That could create another reason for interest rates to move lower.

To see how this plays out in real numbers, compare different home prices in Twikup’s 2026 guide to mortgage payments on $500K, $700K and $1 million homes.

Why Canadian Mortgage Rates Could Stay Higher

This is the other side of the story—and arguably the most important reason Canadians should not automatically assume mortgage rates will continue falling.

1. Oil and Energy Prices Could Keep Inflation Elevated

Canada’s inflation outlook became more complicated in 2026 as higher oil prices pushed energy costs upward.

The Bank of Canada said in June that CPI inflation had risen to 2.8% in April, largely reflecting higher energy prices and the impact of the elimination of the consumer carbon tax dropping out of the 12-month comparison.

The Bank also said core inflation measures had moved closer to 2%.

That creates a difficult situation.

The Bank may want to support a weaker economy.

But it also cannot ignore persistent inflation.

If higher energy prices begin affecting:

- transportation;

- food;

- manufacturing;

- construction;

- airline prices;

- consumer goods,

inflation could become broader.

That would make aggressive interest-rate cuts more difficult.

2. Tariffs Could Hurt the Economy and Increase Prices at the Same Time

Tariffs create one of the most difficult economic situations for central banks.

They can weaken economic growth.

But they can also increase prices.

Imagine Canadian businesses facing higher costs for imported materials or disrupted supply chains.

Businesses may respond by:

- reducing investment;

- cutting jobs;

- raising prices.

That creates a dangerous combination:

a weaker economy with higher inflation.

Economists often describe this broader economic problem as stagflation.

It is one of the most difficult situations for central banks because cutting rates could increase inflation, while raising rates could further damage the economy.

3. Fixed Mortgage Rates Could Remain High Even If the Bank of Canada Cuts

This may be the biggest misunderstanding among Canadian homebuyers.

Suppose the Bank of Canada cuts its policy interest rate.

Many people automatically assume:

“Mortgage rates are going down.”

That is not necessarily true.

Variable mortgage rates generally respond more directly to Bank of Canada policy decisions.

Fixed mortgage rates are heavily influenced by Government of Canada bond yields.

Bond yields can move because of:

- inflation expectations;

- government borrowing;

- global interest rates;

- U.S. bond markets;

- investor sentiment;

- economic growth expectations.

This means the Bank of Canada could lower interest rates while five-year fixed mortgage rates remain relatively expensive.

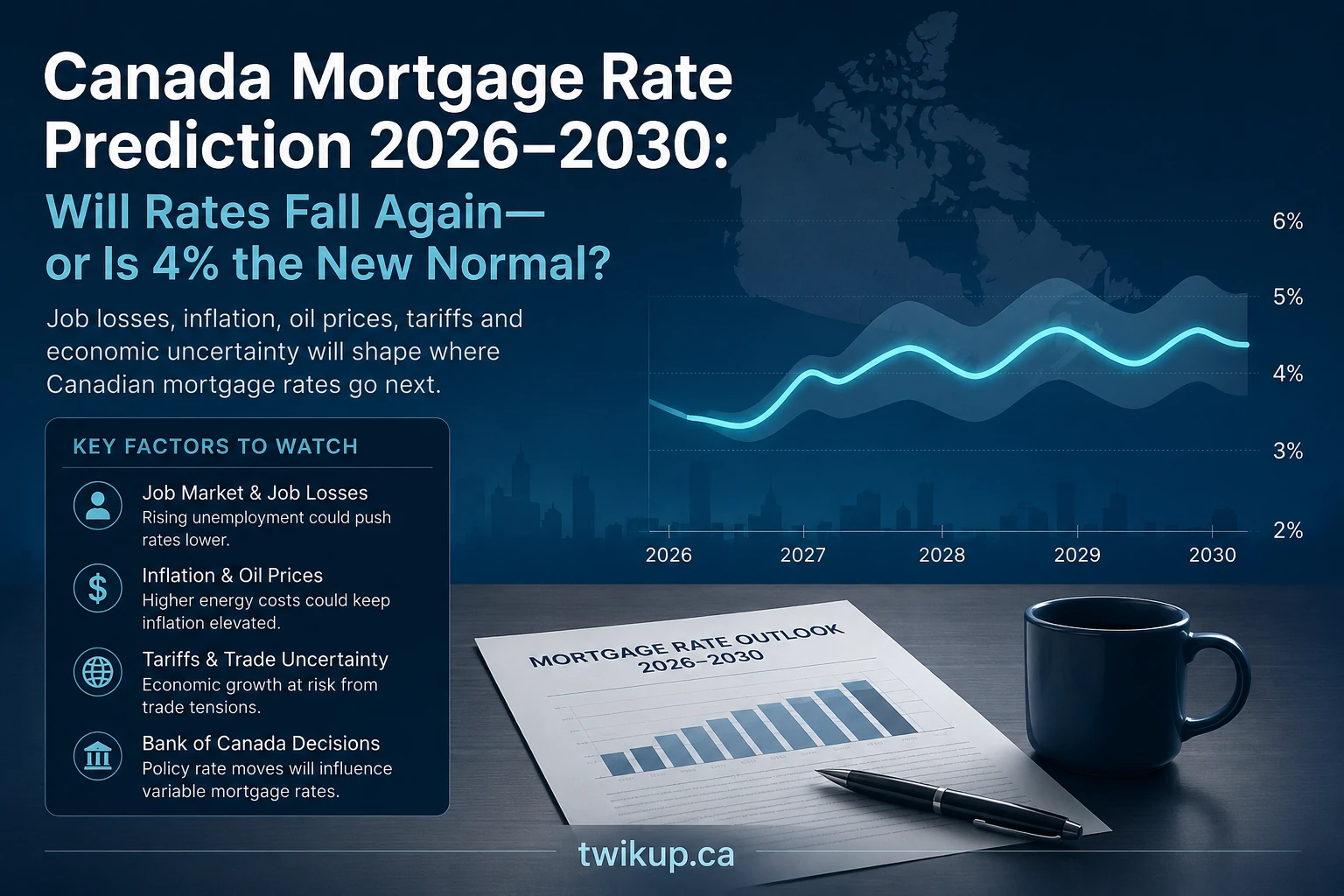

Canada Mortgage Rate Prediction 2026–2030

Predicting exact mortgage rates five years into the future is impossible.

The better approach is to examine the economic conditions that could influence rates.

Here is Twikup’s scenario-based outlook.

| Year | Twikup Base-Case Mortgage Rate Range | Main Factors to Watch |

|---|---|---|

| 2026 | 3.5%–5.0% | Inflation, oil, tariffs, Bank of Canada decisions |

| 2027 | 3.25%–5.0% | Economic growth, inflation returning toward target |

| 2028 | 3.5%–5.25% | Economic recovery and long-term bond yields |

| 2029 | 3.5%–5.5% | Inflation cycle and global economic conditions |

| 2030 | 3.5%–5.5% | Long-term economic growth and monetary policy |

These ranges are scenario-based Twikup estimates, not official Bank of Canada forecasts.

The most important point is not whether a mortgage rate reaches exactly 3.75%, 4.25% or 4.75%.

The larger trend matters more.

Our base case is that mortgage rates fluctuate rather than continuously fall.

If you are comparing this mortgage-rate outlook with where home prices could go, Twikup’s Canada housing market by city prediction for 2026–2031 breaks down the outlook for Toronto, Vancouver, Calgary, Ottawa, Montreal and more.

2026 Mortgage Rate Prediction

Twikup Base-Case Range: 3.5%–5.0%

The remainder of 2026 could be dominated by uncertainty.

Canada faces competing pressures from:

- higher energy prices;

- U.S. tariffs;

- trade uncertainty;

- slow economic growth;

- labour-market risks.

The Bank of Canada may have limited reason to make aggressive moves unless economic conditions change significantly.

Twikup Prediction

Mortgage rates are likely to remain relatively stable but volatile through the remainder of 2026.

Variable mortgage rates could move lower if the economy deteriorates.

Fixed mortgage rates could remain stubbornly high if bond yields stay elevated.

2027 Mortgage Rate Prediction

Twikup Base-Case Range: 3.25%–5.0%

The Bank of Canada expects inflation to gradually move back toward its 2% target in 2027.

If that happens, policymakers could gain greater flexibility.

However, lower inflation does not automatically mean dramatically lower mortgage rates.

Some economic forecasts expect the Bank of Canada policy rate to remain stable, while others see the possibility of rates eventually moving higher as the economy adjusts.

Twikup Prediction

2027 could offer slightly better borrowing conditions, but we do not expect a widespread return to pandemic-era mortgage rates.

2028 Mortgage Rate Prediction

Twikup Base-Case Range: 3.5%–5.25%

By 2028, the immediate effects of today’s economic shocks could become less important.

The focus could shift toward:

- Canada’s productivity;

- economic growth;

- population growth;

- housing construction;

- government debt;

- global interest rates.

If the economy returns to healthier growth, the Bank of Canada may have little reason to maintain unusually low interest rates.

Twikup Prediction

Mortgage rates could begin settling into a longer-term range where approximately 4% no longer feels unusually expensive.

2029 Mortgage Rate Prediction

Twikup Base-Case Range: 3.5%–5.5%

Predicting economic conditions this far into the future becomes increasingly uncertain.

By 2029, Canada could have experienced an entirely new economic cycle.

The country could face:

- stronger economic growth;

- another recession;

- renewed inflation;

- a commodity boom;

- geopolitical disruption.

Twikup Prediction

The most realistic assumption is continued mortgage-rate volatility rather than a straight-line decline.

2030 Mortgage Rate Prediction

Twikup Base-Case Range: 3.5%–5.5%

By 2030, Canadians may have adjusted to a very different mortgage market.

The expectation that mortgages should cost 2% could gradually disappear.

Instead, borrowers may increasingly view rates around 4% as relatively normal.

Twikup Prediction

Unless Canada experiences a major recession or financial crisis, mortgage rates around the 3.5%–5.5% range could represent a reasonable long-term scenario by the end of the decade.

Three Possible Futures for Canadian Mortgage Rates

Because no one can accurately predict interest rates five years in advance, Canadians should consider multiple scenarios.

| Scenario | Possible Mortgage Rate Environment | What Could Cause It? |

|---|---|---|

| Low-Rate Scenario | 2.5%–4.0% | Severe recession, major job losses, very low inflation |

| Base-Case Scenario | 3.5%–5.0% | Moderate growth and inflation near target |

| High-Rate Scenario | 5.0%–7.0%+ | Persistent inflation, energy shocks or global instability |

Scenario #1: Canada Enters a Serious Recession

Imagine unemployment rises sharply.

Businesses cut jobs.

Consumers stop spending.

Housing activity falls.

Inflation drops below target.

Under this scenario, the Bank of Canada could respond with aggressive interest-rate cuts.

Variable mortgage rates could fall quickly.

Fixed mortgage rates could eventually decline as bond yields respond to weaker economic conditions.

Could 2% Mortgage Rates Return?

Possibly.

But it could require a serious economic downturn.

That creates an uncomfortable reality.

The economic conditions required to produce extremely cheap mortgages may also make Canadians less financially secure and less willing to buy homes.

Scenario #2: Canada Avoids Recession but Growth Remains Slow

This is Twikup’s base-case scenario.

The economy continues growing slowly.

Unemployment remains elevated but does not collapse.

Inflation stays relatively close to the Bank of Canada’s target.

Under these conditions, there may be little reason for either dramatically higher or dramatically lower interest rates.

Result?

Mortgage rates could spend much of the next five years fluctuating between approximately 3.5% and 5%.

This is the scenario where 4% mortgages become the new normal.

For homebuyers, this scenario matters because affordability would depend less on waiting for rates to collapse and more on choosing the right market, price point and timing. That is where Twikup’s city-by-city Canadian housing forecast for 2026–2031 can help readers compare regional risk.

Scenario #3: Inflation Returns

Now imagine a very different future.

Oil prices remain elevated.

Global conflicts continue.

Tariffs increase costs.

Supply chains face new disruptions.

Inflation begins rising again.

Under this scenario, the Bank of Canada could be forced to maintain higher interest rates—or potentially increase them.

Fixed mortgage rates could also rise if bond markets expect persistent inflation.

Result?

Canadian mortgage rates could move above 5% again.

In a more severe inflationary shock, rates above 6% could return.

Will 2% Mortgage Rates Ever Return to Canada?

Yes.

But there is an important difference between “possible” and “normal.”

Canada could see mortgage rates near 2% again during extraordinary economic conditions.

For example:

- a severe recession;

- a financial crisis;

- prolonged deflation;

- another major global economic shock.

However, expecting 2% mortgage rates to become the long-term norm may be unrealistic.

The pandemic-era mortgage market was created by exceptional circumstances.

Borrowers should be careful about building their financial plans around the assumption that those rates will automatically return.

Twikup Insight

The biggest mistake Canadians could make is waiting for the Bank of Canada to “bring back” cheap mortgages.

The Bank of Canada is not trying to make homes affordable or mortgages cheap. Its primary monetary-policy objective is maintaining price stability by keeping inflation close to its 2% target over time.

That means the future of mortgage rates could depend on an uncomfortable economic battle.

If unemployment and job losses become the bigger problem, rates could fall.

If oil prices, tariffs and inflation become the bigger problem, rates could stay higher—or rise again.

Our base case is that neither side completely wins.

Canada avoids a deep economic collapse, but inflation risks prevent a permanent return to ultra-cheap borrowing.

That could leave Canadian mortgage rates fluctuating around 3.5% to 5% for much of the remainder of the decade—making roughly 4% mortgages less of a temporary problem and more of a potential new normal.

Should Canadians Wait for Mortgage Rates to Fall Before Buying a Home?

This is where mortgage predictions become dangerous.

A buyer could wait two years for mortgage rates to fall—only to discover that home prices have increased.

Alternatively, someone could rush into the housing market expecting rates to fall—and discover that borrowing costs remain elevated.

There is no perfect strategy based entirely on interest-rate predictions.

Instead, potential buyers should consider:

- whether they can comfortably afford the monthly payment;

- emergency savings;

- job stability;

- other debts;

- expected ownership period;

- maintenance and property costs;

- the possibility of higher renewal rates.

The best mortgage rate prediction cannot compensate for buying a home that is unaffordable.

For a broader view of whether Canadian home prices may rise or fall over the next five years, read Twikup’s full Canada real estate price prediction for 2026–2031.

What Does This Mean for Canadians Renewing a Mortgage?

Homeowners approaching renewal face a different decision.

The most important question may not be:

“Will rates fall?”

It may be:

“How much financial flexibility do I need if the prediction is wrong?”

Canadians renewing a mortgage may want to compare:

- fixed versus variable rates;

- shorter versus longer mortgage terms;

- prepayment privileges;

- penalties;

- refinancing costs;

- monthly cash-flow requirements.

A borrower who expects rates to fall may prefer greater flexibility.

A borrower who prioritizes predictable payments may prefer the certainty of a fixed mortgage.

The right choice depends on personal financial circumstances rather than a single interest-rate prediction.

What Could Make This Mortgage Rate Prediction Wrong?

Every long-term economic prediction should clearly explain what could invalidate it.

Our outlook could change significantly if Canada experiences:

- a severe recession;

- a rapid increase in unemployment;

- another financial crisis;

- unexpectedly persistent inflation;

- dramatically higher oil prices;

- major changes in U.S.-Canada trade relations;

- geopolitical conflicts;

- large changes in government borrowing;

- another global economic shock.

That is why Canadians should treat mortgage-rate forecasts as scenarios rather than promises.

Final Prediction: Is 4% the New Normal?

Possibly.

But the bigger story is that Canadians may need to stop expecting mortgage rates to move in only one direction.

Between 2026 and 2030, the Bank of Canada could face an ongoing battle between two competing problems.

A weak economy and job losses could push interest rates lower.

Oil shocks, tariffs and inflation could push rates higher.

The most realistic outcome may lie somewhere between these extremes.

Twikup’s 2026–2030 Base Case

Canadian mortgage rates could spend much of the remainder of the decade fluctuating between approximately 3.5% and 5%.

Rates below 3% remain possible during a serious economic downturn.

Rates above 5% remain possible if inflation returns.

But without a major economic crisis or inflation shock, mortgage rates around 4% could increasingly become Canada’s new normal.

The era of ultra-cheap money may not be gone forever.

But Canadians should think carefully before building their financial future around the assumption that it is coming back.

Frequently Asked Questions

Will Canadian mortgage rates fall in 2026?

Mortgage rates could fall if the Canadian economy weakens significantly or the Bank of Canada reduces its policy rate. However, fixed mortgage rates also depend heavily on bond yields, meaning they may not decline at the same pace as variable rates.

What is the Canadian mortgage rate prediction for 2027?

Twikup’s scenario-based base-case range for 2027 is approximately 3.25% to 5%, depending on inflation, economic growth, Bank of Canada policy and bond-market conditions.

Could mortgage rates return to 2% in Canada?

Yes, but a return to mortgage rates around 2% could require extraordinary economic circumstances, such as a severe recession or financial crisis. Twikup does not consider 2% mortgages the most likely long-term base case.

Will 4% mortgage rates become normal in Canada?

It is possible. If Canada experiences moderate economic growth while inflation remains close to the Bank of Canada’s target, mortgage rates could fluctuate around the 3.5% to 5% range for extended periods.

What causes mortgage rates to fall in Canada?

Mortgage rates can fall because of lower Bank of Canada policy rates, declining bond yields, weaker economic growth, lower inflation expectations or increased competition among mortgage lenders.

What could cause Canadian mortgage rates to rise again?

Persistent inflation, higher energy prices, stronger-than-expected economic growth, rising bond yields, global instability and supply-chain disruptions could put upward pressure on mortgage rates.

Does the Bank of Canada control mortgage rates?

Not directly. Bank of Canada policy decisions strongly influence variable mortgage rates through lender prime rates. Fixed mortgage rates are more heavily influenced by Government of Canada bond yields and lender funding costs.

Should I wait for mortgage rates to fall before buying a home?

That depends on your finances, job stability, housing needs and ability to comfortably afford the mortgage. Future interest rates are uncertain, and waiting for lower rates can create other risks, including the possibility of changing home prices.

Last updated: July 2026.

Sources and methodology: This article is based on publicly available information from the Bank of Canada, Statistics Canada and current Canadian mortgage-market data. Future mortgage-rate ranges are scenario-based Twikup analysis and are not official forecasts from the Bank of Canada or any financial institution.

Disclaimer: This content is for general informational and educational purposes only and does not constitute financial, mortgage, investment, legal or tax advice. Mortgage rates, qualification requirements and economic conditions can change. Consider consulting a qualified mortgage professional or financial adviser regarding your individual circumstances.